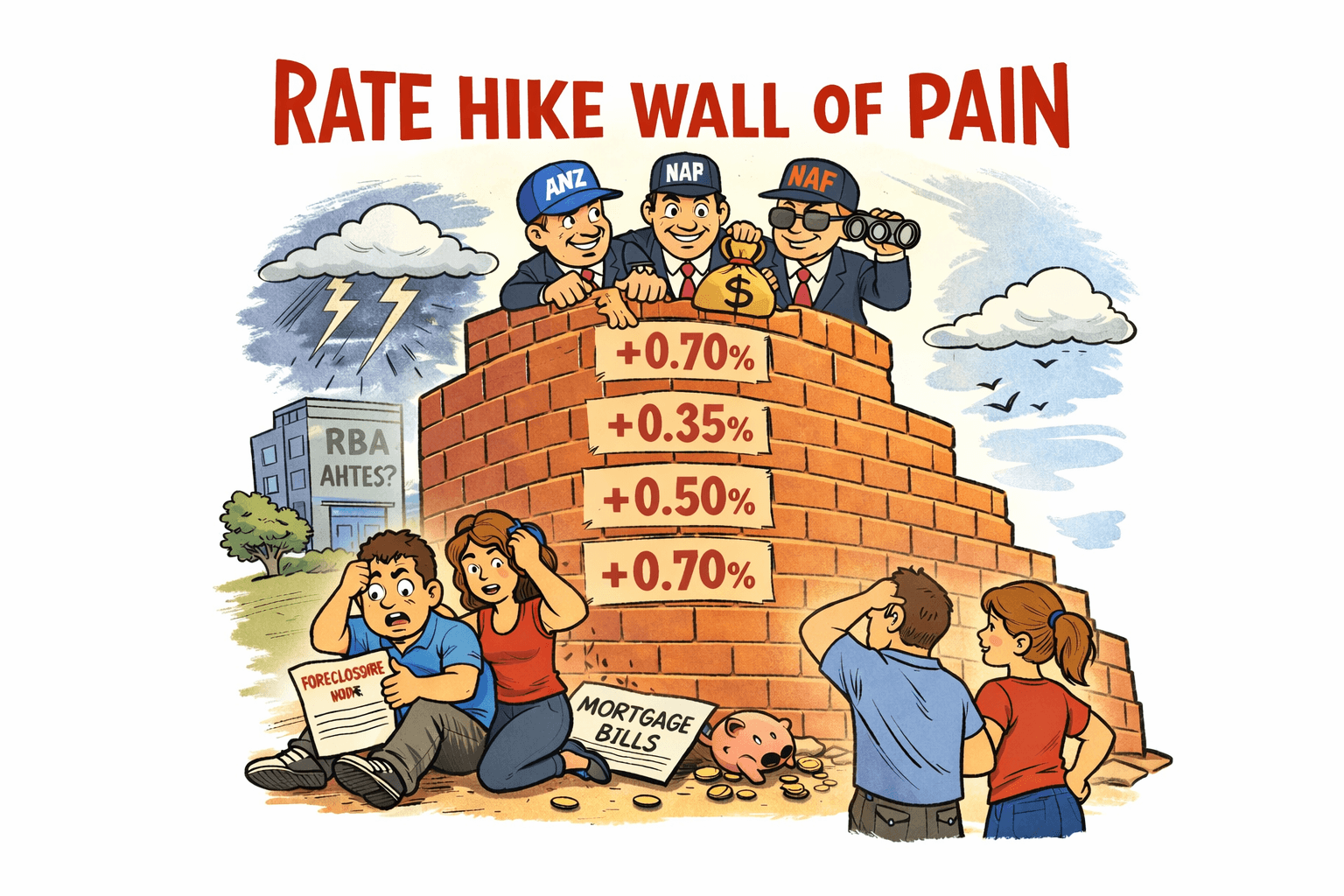

Rate Hikes Galore: The Great Wall of Pain

Banks have decided that compassion is out and rate hikes are in. A whopping 53 lenders have pushed fixed home loan rates higher since the RBA’s last meeting, and this includes all the heavyweights — ANZ, NAB, Westpac and their merry offshoots. They’re now jogging interest prices up by as much as 0.70 percentage points on some products, which feels like a tactical retreat from borrowers’ wallets. Meanwhile, two lenders have even begun lifting variable rates, a sneak attack that suggests lenders are nervously prepping for more RBA tightening in February.

This isn’t a tiny shuffle; it’s a full-blown repricing blitz that turns any hope of refinancing into an exercise in emotional damage control. Despite brand economists muttering about “pre-emptive moves,” most market pricing still suggests RBA cuts are more likely than hikes. So it’s hard to know whether banks are clairvoyant or just betting on borrowers’ despair.

Mortgage Demand: Boom or Bubble?

Yet, in some corners of the country, credit demand looks positively exuberant. Mortgage enquiries have surged to their highest level in three years, powered by rate cuts last year, juicy first-homebuyer incentives and rent inflation that looks like a goat on steroids. Queensland, WA and NSW are leading this charge, with buyers either chasing dreams or fleeing rent carnage.

The big four banks are the biggest beneficiaries of new home loan searches, while a healthy tranche of the refinance crowd is also out there hunting better deals. To call this a paradox would be polite: in one hand we have crushing repayment pain; in the other we have buyers doubling down on debt like it’s a clearance sale.

SME Insolvencies: Non-Banks at the Helm

The corporate undercurrent is grinding too. Insolvency pressures on SMEs are climbing, and guess who’s driving most of the courtroom dustups? Non-bank lenders. These new-age credit beasts are now leading the charge in court-enforced recoveries, stepping in where traditional banks have quietly stepped back.

That’s not exactly comforting if you’re an SME trying to stay solvent; it’s like being chased by a pack of accountants with clipboards and zero mercy. The shift suggests majors are reining in risky lending while nimble challengers are going to town on enforcement. Borrowers beware: the new sheriff in town carries a very different badge.

Branch Closures: The Retail Banking Retreat

Meanwhile, People First Bank — a customer-owned institution — is pulling back from the high street, closing 15 branches and three agencies. The official line is that digital banking is killing foot traffic and the cuts are about “better service.” But let’s translate: when less than 1% of transactions happen in branches and your business model depends on people still walking through doors, it’s not innovation — it’s retrenchment.

This is the sterile future of banking: more apps, fewer smiles. For regional customers, especially those who still think ATMs are a marvel, that’s a downgrade disguised as progress.

Wall Street Meets Aussie Shores

Over at Citi, the bankers are celebrating like it’s 1999. Bonuses jumped 20% for Australian dealmakers — proof that while everyone else is fretting over mortgage shock, finance elites are still having their cake and eating it with tax-efficient gusto. That kind of disconnect is the financial sector’s unofficial national sport.

But don’t get too comfortable: cuts to costs are reportedly on the table. Translation: bonus increases today, efficiency layoffs tomorrow. It’s an impressive one-two punch of capitalism living its best life.

Public Bank? Some Councils Say “Why Not?”

Out in Wagga Wagga, local councillors are ringing alarm bells about the banking status quo and urging Canberra to set up a government-owned bank. Yes, that old chestnut is back. Whether it’s serious policy or political theatre, it reflects escalating frustration with big banking’s blend of high costs and low empathy.

A public bank would be pitched as more community-focused, but let’s be honest: if banking was ever going to be driven by altruism, the RBA’s cash-rate calls would come with a side of therapeutic Lego.

In Summary

Rate rises, frenzied borrowing, non-bank muscle, branch closures and bonused bankers — the 2026 financial carnival has marvellous attractions for everyone except the average Australian. In other words, your wallet’s favourite pastime this year will be watching the financial sector do exactly what it always does: make money, cause pain, and call it progress.