Rising Rate Rage

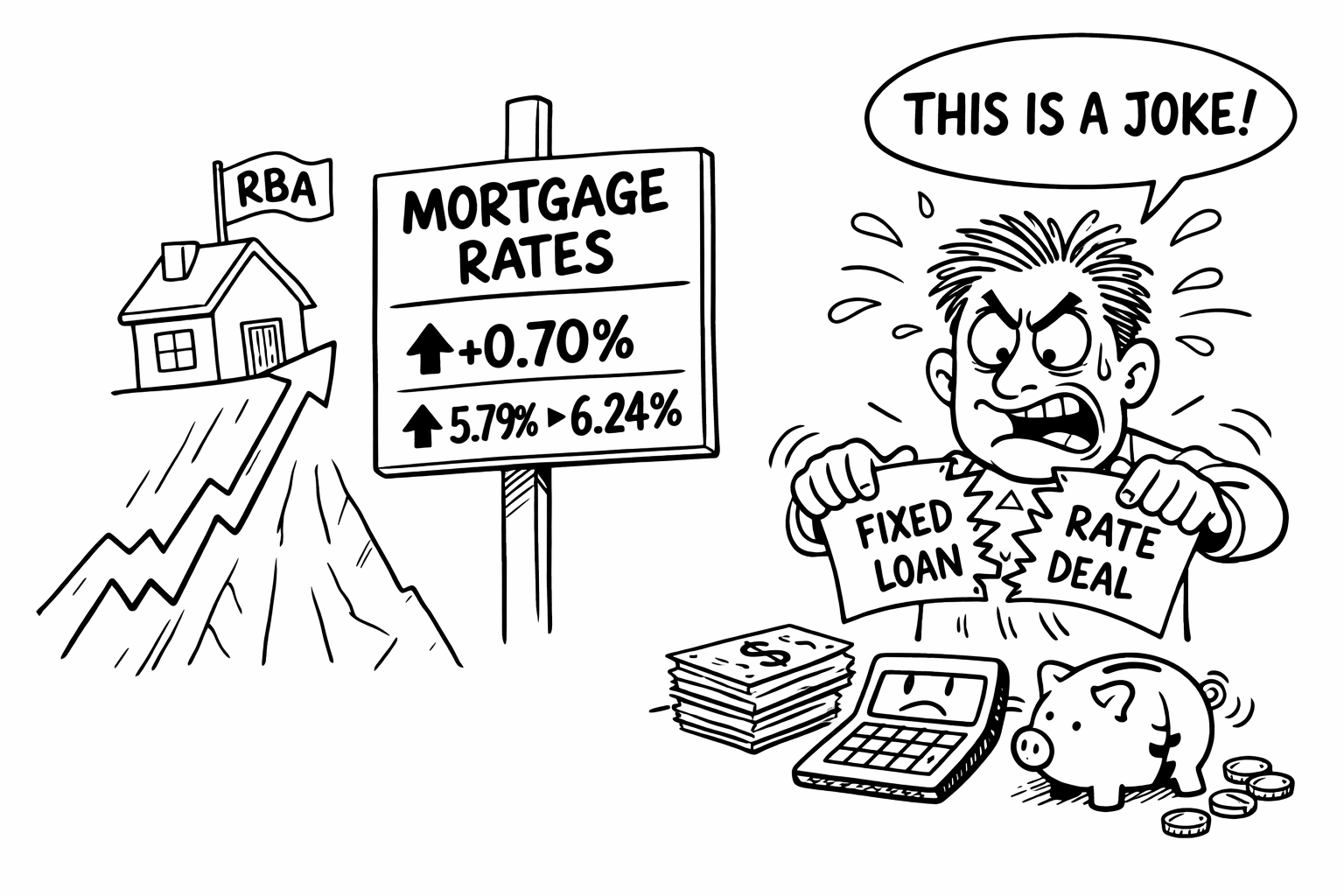

Australia’s mortgage market got a fresh reminder that banks only make money when you don’t. On Thursday, Commonwealth Bank and Macquarie Bank both lifted fixed home-loan rates, with CommBank hikes as high as +70 basis points and Macquarie also pushing its lowest fixed offers markedly higher. Lenders are telegraphing their own forecasts: if they see trouble coming from the Reserve Bank of Australia’s next meeting — tipped for an early-February rate hike — you’ll see it in your repayments first.

CommBank now advertises its lowest fixed rates around 5.79%-6.24% for owner-occupiers, an astonishing reversal from the sub-5% specials we saw mid-2025. Macquarie’s comparable offers have crept toward the 5.5%+ range depending on loan size and term. If you’re a hopeful homeowner clutching a fixed-rate deal from six months ago like a winning lotto ticket, you’re now living in a different world — one where price competition means who can charge more this week.

Chiefs Leaving/Back Office Wilting

It’s not just retail customers feeling squeezed — internal morale is cracking too. Commonwealth Bank’s vaunted “star” home-loan unit has lost its chief under murky circumstances, with more than 20 senior lenders departing last month alone. For a bank that once touted its proprietary mortgage machine as a strategic advantage, this exodus reads like a resignation letter from reality.

What does this mean for borrowers? Less negotiation talent on your side — and more incentives for banks to push customers toward their own products or expensive servicing channels rather than low-cost mortgage solutions. The internal churn suggests that big banks are beginning to feel the pain of tighter margins and heightened competition from non-bank lenders and brokers.

Investor Loans: Peaks and Plateaus

While mortgage rates are climbing, investors are not sitting quietly either. New data shows investor loan numbers have hit fresh records, with more than 205,000 new investor mortgages written in the past year — a 9% annual rise that eclipses previous peaks. Victoria and NSW are the key battlegrounds, with Victoria’s investor lending growth now outpacing Queensland’s as affordability narratives shift.

Queensland’s investor demand, in contrast, has slowed from last year’s torrid pace — still positive but lagging the national trend — while owner-occupier loan values keep climbing, underscoring how the home-buying market feels like a game of musical chairs where investors swipe prime spots first.

Branches Not Profits

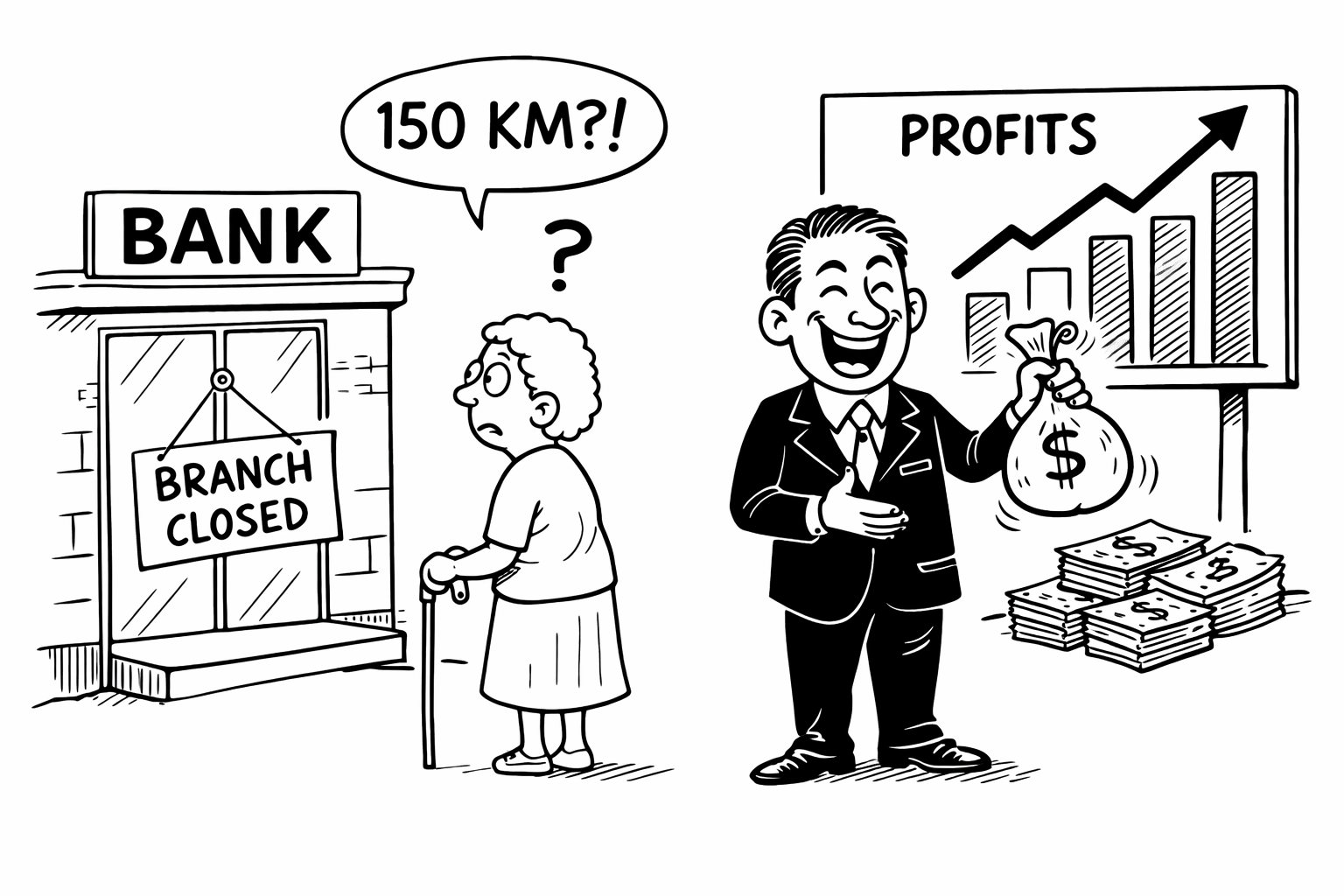

Small bank, big betrayal. People First Bank — formed from the merger of Heritage Bank and People’s Choice Credit Union — has announced it will close 15 more branches across regional Australia, including in Queensland, NSW, Victoria and South Australia. Towns such as Oakey and Pittsworth will be left without any physical banking services, forcing customers to drive up to 150 km for in-person access.

This closure spree flies in the face of boffins who once claimed community banking put people first. Less than 1% of transactions now occur in branch, the bank protests — yet profits climbed 7% last year. Ordinary customers who aren’t comfortable with apps, digital wallets, and chatbot support? Tough luck.

The Credit Card Cap Question

The international debate du jour: should Australia copy the U.S. and cap credit card interest at 10%? Right now, there’s no cap here at home — rates are set by market competition, meaning cards regularly charge 17–21% or more, based mainly on credit risk and income profiles.

Proponents of a cap argue it could ease household debt burdens, especially for those dragging balances month-to-month. Critics — including some economists — warn a cap that’s too low could shrink access to credit, pushing borrowers toward even more expensive alternatives. The policy debate is heating up, but for now banks keep charging whatever the market will bear.

Banks Want a Safety Net Too

While households sweat every basis point, big banks have their own hands out. The influential banking lobby is pushing for the Compensation Scheme of Last Resort to be reshaped with means testing, rather than being a broad collective bailout for investors when misconduct wrecks customer outcomes. They argue that fully funded collective payouts go beyond the original intent, potentially extending to hypothetical gains instead of actual losses.

If that sounds like banks complaining about liability for their own misdeeds — it is. But in Canberra’s current spin ecosystem, even that argument somehow gets couched in terms of “fairness” and “budgeting”

Summary

So here’s the picture: loan rates ascending like bad inflation jokes, once-star bankers fleeing to greener broker pastures, investors acting like it’s Boxing Day at Sotheby’s, regional Australia being told to Uber to their nearest branch, and credit card users still having their pockets picked with dazzling consistency. Oh — and banks are now lobbying to make it harder for you to get paid when they screw up. If finance were any funnier, it’d be illegal.