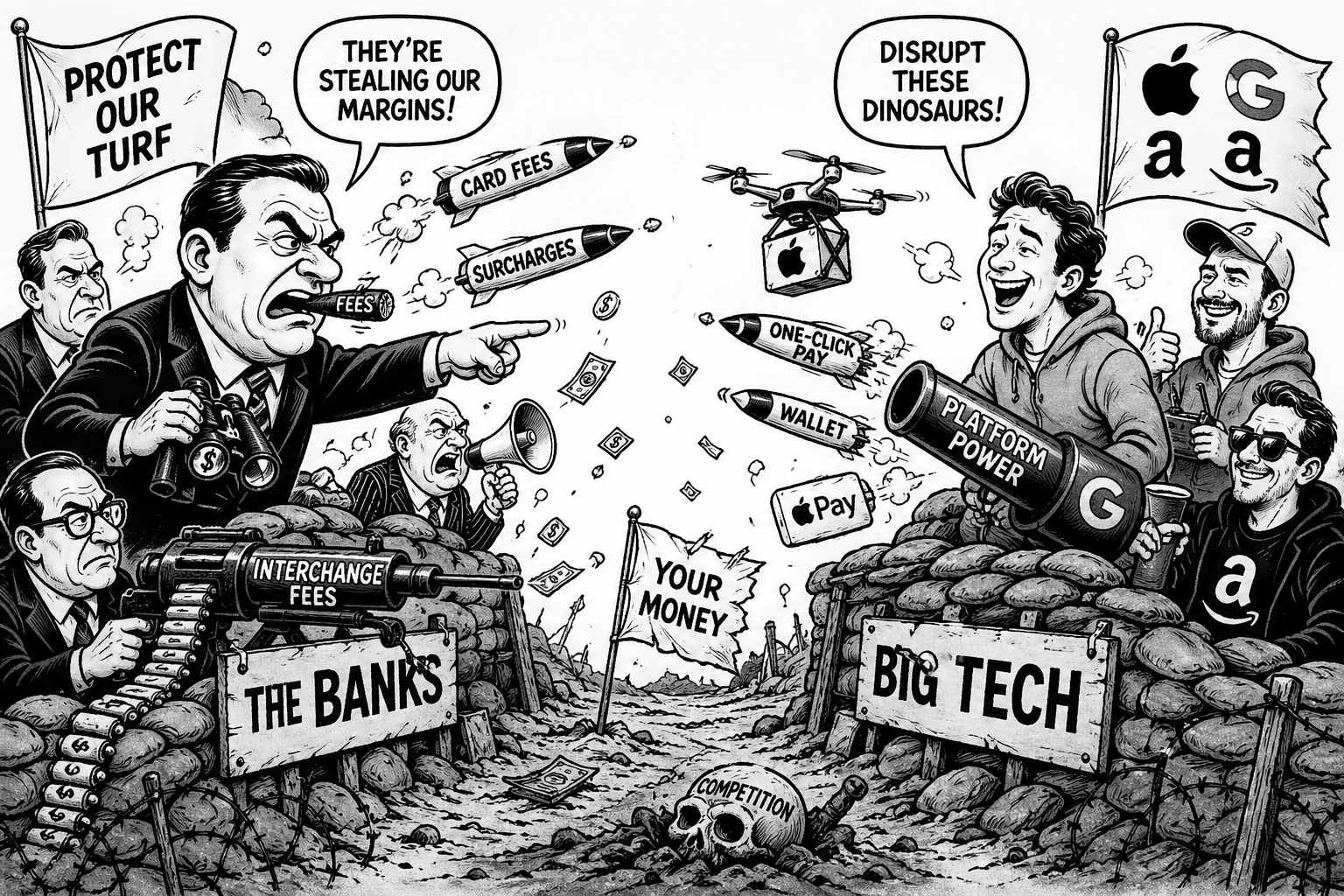

Banks vs big tech: $16b tantrum

Australia’s banks have decided Big Tech isn’t paying its “fair share” — and by fair share, they mean roughly $16 billion in card fees. The argument? Tech giants like Apple and Google sit between banks and customers, quietly clipping the ticket.

The banks want regulatory intervention to level the playing field. Translation: “We’d like the monopoly back, thanks.” It’s less David vs Goliath and more Goliath vs slightly shinier Goliath.

Bots policing bots

Commonwealth Bank has rolled out new AI tools to combat a surge in mortgage fraud — much of it allegedly powered by AI-generated fake documents.

So we now have AI committing fraud and AI detecting fraud. Humanity’s role? Standing awkwardly in the middle, holding a clipboard and pretending we’re still in charge.

Rate hikes: Because once isn’t enough

The Reserve Bank may not just raise rates — it could go the full double-tap. Economists are floating the idea of back-to-back hikes if inflation refuses to behave.

Nothing says “cost of living relief” like doubling your mortgage pain in stereo.

Firing line for finfluencers

Australian Securities and Investments Commission is cracking down on finfluencers who’ve been dishing out financial advice like it’s protein powder — loosely measured and potentially harmful.

Turns out disclaimers like “not financial advice” don’t legally transform bad advice into performance art.

Westpac leads the pack

Westpac has lifted interest rates across multiple products, proving once again that banks don’t need the RBA’s permission to make your life more expensive.

Funny how rate cuts require deep reflection, but hikes arrive like Uber Eats — fast and unapologetic.

Lesson learned?

The Federal Court has ordered Money3 to pay $1.55 million for breaching responsible lending laws.

In banking terms, it’s not so much a punishment, more a moderately inconvenient rounding error. Still, it’s a reminder that “responsible lending” isn’t just a vibe.

Bean counter busted

An accountant has been charged as authorities investigate a suspected $3 billion mortgage fraud scheme.

It’s the kind of number that makes you wonder if “verification process” was just a polite suggestion.

Short URL: https://bit.ly/3Fraud3B

Australia’s biggest lender

A new survey shows 34% of Australians need help from family to buy a home.

At this point, the Bank of Mum and Dad isn’t a safety net — it’s the entire housing finance system with better customer service and no formal complaints process.

Free money? Unlikely.

Banks are dangling cashback offers to lure borrowers — thousands upfront, in exchange for years of higher repayments.

It’s like being paid to walk into a maze. Sure, you get cash now. But the exit gets further away every month.

Wisr gets its wish

Wisr has hit a $1 billion loan book after a 68% surge in originations.

Credit growth is booming — which is fantastic, right up until the repayments start arriving with the enthusiasm of a debt collector on commission.

Retirement’s last resort

By many accounts the demand for reverse mortgages is rising, driven by younger retirees looking to unlock equity.

In other words, people are retiring earlier — and then borrowing against their homes to afford it. Retirement planning now includes “hope the house holds up.”

In summary

Banks get grumpy, regulators fire shots, fraudsters become more creative, and borrowers just want a break — preferably one that doesn’t come with interest attached. The system isn’t broken; it’s working exactly as designed. That’s the worrying part.