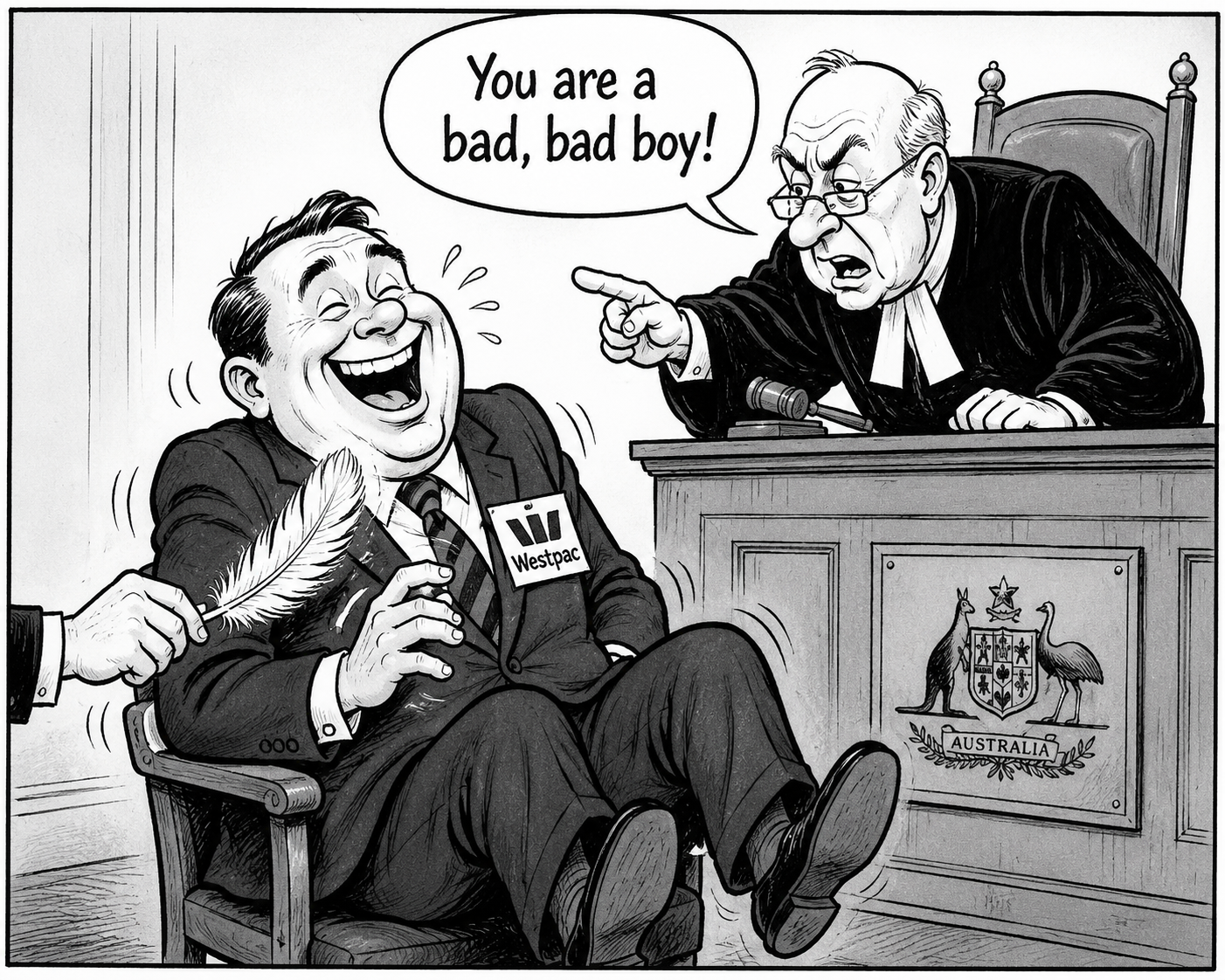

Westpac’s $26 million oopsie

ASIC successfully secured a $26 million penalty against Westpac over failures in handling customer hardship applications. Thousands of struggling customers were affected. The bank failed to properly process requests from people already drowning financially. Which is a little like a lifeguard outsourcing CPR to voicemail.

Westpac admitted issues with hardship notices and delays affecting vulnerable customers between 2015 and 2022. Seven years. In corporate terms, that’s less “isolated incident” and more “operating philosophy”.

Still, $26 million for a major bank is roughly equivalent to fining a cruise ship captain one prawn from the buffet.

Scam refunds: Britain hands out $150,000. Australia offers a bus fare.

Australia is preparing a scam reimbursement scheme where victims could receive up to $3,000 quickly if banks fail to meet anti-scam obligations. In the UK, victims can receive compensation closer to A$150,000. Which is one way of revealing how seriously each country treats financial crime. Britain says: “This ruined your life.” Australia says: “Here’s enough for a replacement iPhone and perhaps a consoling schnitzel.”

The proposal follows years of banks and telcos treating scam prevention like a workplace wellness seminar: plenty of PowerPoint slides, no meaningful outcomes. Australians lost billions to scams last year, while regulators discovered that “please be careful online” wasn’t quite the iron dome they’d hoped for.

The banking industry, naturally, is worried about “moral hazard”, which is finance-speak for: “We’d hate to accidentally help customers.” The Conversation

Banks rewrite the rules before Parliament does

More lenders have updated their serviceability calculators to strip negative gearing benefits from investor loans on established properties — despite the fact that the legislation hasn’t passed, the Senate hasn’t voted, and technically nothing has changed under law.

The practical effect is that investors relying on negative gearing to boost their serviceability are discovering their borrowing capacity has quietly shrunk before a single parliamentary vote has been cast. Banks have decided that since the change is “foreseeable,” they might as well price it in now — which raises the mildly interesting question of what the point of legislating anything is if the lending industry simply acts on proposals the moment a Treasurer sits down. Responsible lending, absolutely. Democratic process, a minor inconvenience. Broker Daily has more

Bank fees: The RBA discovers banks enjoy charging people

The Reserve Bank released fresh analysis showing Australians still pay billions in bank fees annually, although competitive pressure and digital banking have reduced some charges over time. Translation: banks no longer charge you to look at your own money, which apparently qualifies as progress.

Households pay fewer transaction fees than they once did, largely because banks discovered it’s easier to monetise people invisibly through margins, spreads and mortgage pricing instead. Meanwhile, business banking fees remain stubbornly healthy because small businesses occupy a unique economic category known as “captive prey”. The RBA Bulletin has more detail

Mortgage fraud ring: Apparently “creative lending” has limits

ASIC has charged a former broker and a former banker over an alleged mortgage fraud involving fake documents and fraudulent loans worth millions of dollars.

Authorities allege the man helped a criminal syndicate obtain loans of more than $25 million and the woman submitted close to $13 million dollars in loans using fabricated documents.

In fairness, inflated property valuations and optimistic borrowing assumptions are already standard industry wallpaper, so fake paperwork probably didn’t stand out immediately.

Interest rates: Economists detect economy is slightly on fire

Major banks are making competing RBA predictions with the confidence of astrologers reading goat entrails.

Markets spent two years insisting rates needed to rise because inflation was rampant, then immediately pivoted to panic once consumers stopped spending money they no longer had. Economists now talk about achieving a “soft landing”, a phrase usually heard moments before your luggage catches fire. Here’s Canstar’s take

Brokers told to call customers before customers escape

640,137 Australian home loans were renegotiated or switched in 2025 — about 20% more than the year before. A majority moved to a different lender. The Ipsos Issues Monitor found that 63% of Australians name cost of living as their primary concern — and they are no longer just worried.

Borrowers are shopping aggressively for savings because loyalty to banks has collapsed entirely. Australians now switch lenders with the emotional attachment normally reserved for petrol stations.

The message to brokers is blunt. Ring your clients before another broker does. Romance is alive and well in Australian finance.

CommBank’s AI loan assistant: Finally, a robot to reject you faster

Commonwealth Bank unveiled an AI-powered business loan assistant designed to help small businesses navigate lending applications because when Australians said banking lacked warmth and humanity, the obvious solution was clearly more algorithms.

CBA says the technology will streamline processes and improve customer experience and nothing says “premium banking relationship” like receiving automated rejection messages with machine-learning efficiency.

Still, there’s a brutal honesty to AI banking. At least a robot denying your loan doesn’t pretend to care about your weekend plans first.

Billboard budget: Democracy by outdoor advertising

Sydney mortgage broker Joseph Daoud spent $17,500 on billboard ads at Canberra Airport attacking proposed capital gains tax changes, arguing ambitious Australians “aren’t being listened to”. Which is one way to communicate with politicians. Another would be carrier pigeon. Probably equally effective.

Spending nearly eighteen grand to tell Canberra something it has already ignored repeatedly is either principled advocacy or performance art with GST attached. Possibly both.

So, there it is

Another week in Australian finance: the banks say sorry, the regulators promise lessons will be learned, and ordinary people quietly update their spreadsheets and blood pressure medication.