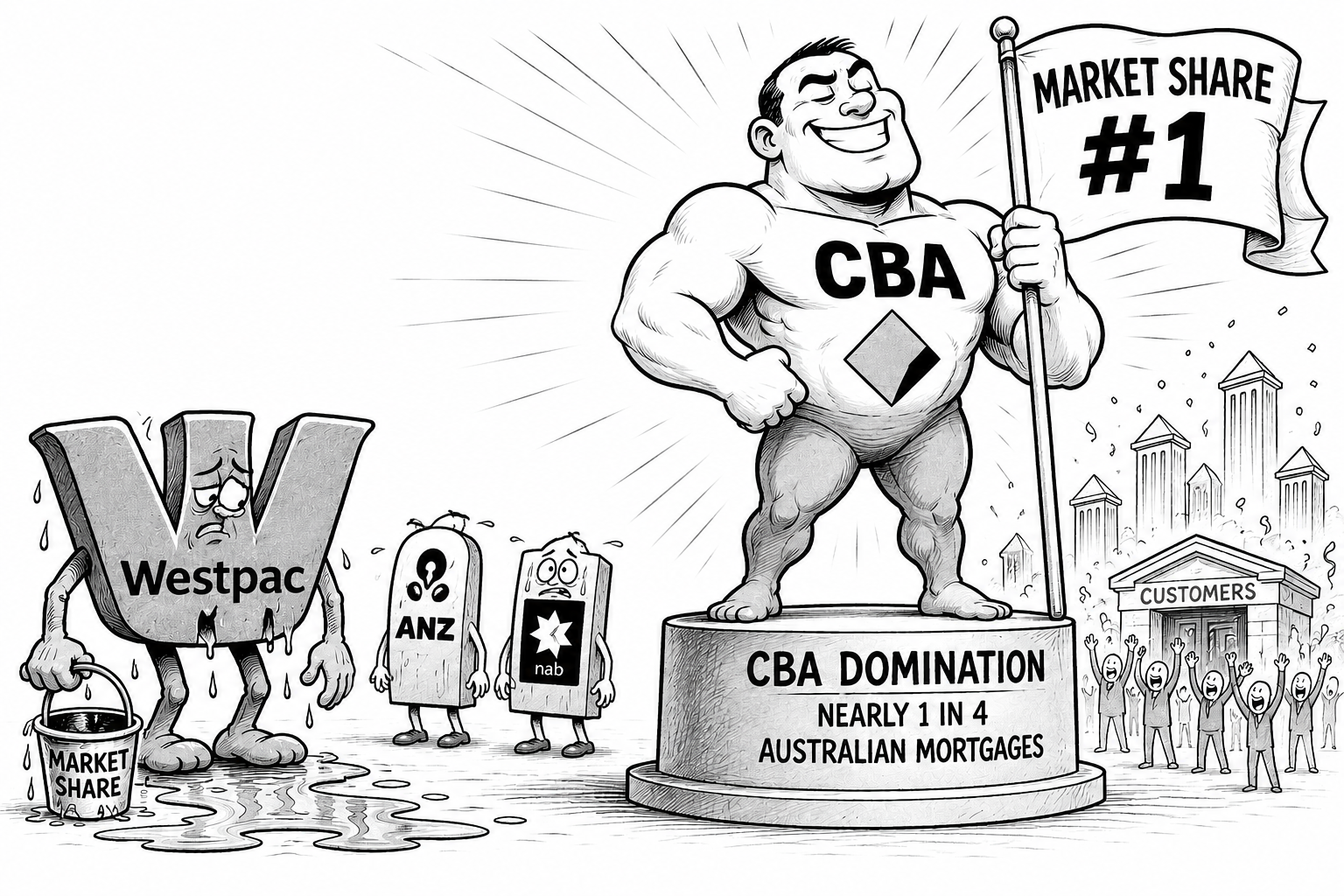

Domination continues

According to mortgage market data, Commonwealth Bank continues to dominate the home lending landscape writing one in four Australian mortgages, which is impressive in the same way a python dominating a bird cage is impressive.

Meanwhile, Australia’s oldest bank is currently discovering that nostalgia is not a business strategy.

Westpac is leaking customers like a rental property leaks mould. It’s share of the market has dropped 3.2 percent since 2019.

The problem for Westpac is brutally simple: scale wins. CBA has the tech, the broker relationships, the pricing power and — perhaps most importantly — the ability to make Australians feel vaguely safe while taking on 30 years of debt at interest rates that resemble a punishment from medieval clergy. In banking, “customer loyalty” mostly means “my direct debit setup is annoying to change”.

Rate rises: The pain persists

Australian banks wasted absolutely no time passing on the latest Reserve Bank of Australia rate rise to borrowers in full. Funny how that efficiency disappears when rates go the other direction. Then suddenly everyone needs “careful assessment of funding conditions”, which is corporate language for “we’d quite like to keep the money”.

The major lenders confirmed mortgage increases almost immediately, ensuring households already being slowly crushed by groceries, insurance and electricity bills can now enjoy the added thrill of watching their monthly repayments rise again.

Banks insist these decisions are necessary. Of course they do. Cigarette companies once insisted doctors recommended menthols.

Macquarie feasts on the Big Four

Macquarie Bank continues nibbling away at the dominance of the major banks. Australians increasingly appear willing to abandon the traditional banking giants in favour of whoever offers a slightly lower rate and an app that doesn’t resemble a government website from 2007.

Macquarie’s rise highlights an uncomfortable truth for the majors: customers are not emotionally attached to banks. Nobody’s sitting around a barbecue saying, “I just love the heritage and values of my variable-rate lender.” People want cheaper repayments and fewer reasons to scream into a pillow.

AI fraud: Here comes the hit list

Australian banks are reportedly compiling a hit list of suspicious mortgage brokers they no longer want to work with. This comes amid growing fears around AI-assisted fraud.

The concern is that generative AI tools are making fake payslips, altered bank statements and synthetic identities easier to produce. Naturally, the response from banks has been to increase surveillance and scrutiny — not of themselves, obviously, but of brokers. Because in every financial crisis, someone slightly lower down the food chain must be sacrificed to preserve executive bonuses.

Sydney’s mortgage delusion

Sydney households are reportedly being pushed “to the edge” by rising interest rates. Which edge specifically remains unclear because Sydney property prices removed all known edges years ago and replaced them with negative equity and artisanal cafes.

The latest warnings suggest more borrowers are approaching mortgage stress as repayments climb. And yet property values somehow continue levitating like a spiritually enlightened balloon. Australia’s housing market remains one of the few places on earth where everyone agrees prices are absurd, unaffordable and unsustainable — immediately before bidding another $300,000 over reserve.

Builders discover consumers have feelings

The construction sector is now confronting not only rate hikes but a worsening “sentiment shift”. Translation: people have stopped confidently signing enormous contracts because they’ve noticed money can, in fact, run out.

Builders are being warned to monitor both financial conditions and consumer psychology as demand softens. This is the inevitable hangover after years of ultra-cheap money convinced Australians that property prices only travel in one direction and builders could charge whatever they liked as long as they added the word “luxury” to the brochure.

Sentiment matters because housing markets are basically confidence games with splashbacks. Check out an interesting analysis at The Good Builder.

Fact Check: The Loan Scheme That Never Was

Fact Check: The loan scheme that never was

Finally, Australian Associated Press fact-checkers debunked viral social media claims about a supposed migrant home loan scheme. The alleged policy — widely shared online — simply does not exist.

But the rumour spread rapidly because modern economic anxiety desperately wants a villain. When housing becomes unattainable, wages stagnate and living costs soar, conspiracy theories flourish in the cracks left by institutional failure. It’s easier to believe in secret schemes than admit the housing market has been systematically broken for decades by governments terrified of upsetting homeowners.

Social media now functions as a national pub conversation, except everyone’s drunker and nobody gets cut off.

The wrap

So here we are: The big banks are consolidating power, AI is industrialising fraud, and mortgage stress is becoming a national personality trait – life on Money Road.